The convergence of advanced robotics and biocompatible materials has effectively bridged the gap between mechanical engineering and human biology, turning what was once science fiction into a standard of clinical care. This evolution represents one of the most sophisticated frontiers of modern medicine, where surgically integrated devices transition from passive mechanical supports to active, data-driven systems that communicate directly with healthcare providers. As of 2026, the global landscape for these life-altering technologies has surpassed a significant valuation, reflecting a profound shift toward value-based care and the seamless integration of digital health solutions into everyday clinical practice. The scope of this industry is remarkably broad, covering everything from cardiovascular pacemakers that synchronize heart rhythms to complex neurostimulators that manage chronic pain and orthopedic joints designed to restore mobility to an aging population. This sector is characterized by rigorous engineering standards and an increasingly complex regulatory environment, yet the potential for improving patient outcomes remains the primary catalyst for ongoing innovation. As researchers and engineers continue to push the boundaries of biocompatibility and wireless connectivity, the medical community is witnessing a departure from traditional hardware toward personalized, biologically intelligent systems.

Economic Outlook: Financial Projections and Market Trajectories

Market Valuation: Understanding the Path to 2034

The financial prospects for the implantable medical devices market are remarkably strong, with the global valuation expected to climb steadily from its current 2026 baseline of approximately $110.94 billion. Experts project a consistent upward momentum, driven by a global healthcare environment that increasingly prioritizes advanced surgical interventions and long-term patient outcomes over temporary treatments. This growth is not merely a reflection of higher sales volumes but also the increased value of sophisticated technologies that offer proactive health management. As implants incorporate internal sensors and wireless connectivity, their therapeutic impact increases, justifying a higher average selling price and deeper market penetration. Investors are increasingly drawn to this stability, recognizing that the demand for life-sustaining and mobility-restoring technology remains resilient even during periods of broader economic volatility.

By the time the industry reaches 2034, the total market size is anticipated to expand to approximately $179.37 billion, representing a robust compound annual growth rate of 6.19%. This expansion is underpinned by significant capital investments in research and development, particularly in the areas of bioelectronics and regenerative medicine. The transition from simple mechanical replacements to complex electronic systems has fundamentally altered the revenue models for major manufacturers, moving toward service-based monitoring and recurring data analytics. This economic shift ensures that the industry is not just selling a physical product but an ongoing clinical outcome. The integration of artificial intelligence and machine learning into the device ecosystem further bolsters this valuation, as these technologies provide the necessary data to reduce hospital readmission rates and improve the overall efficiency of healthcare delivery systems worldwide.

Regional Performance: Global Economic Contributions

Regional performance mirrors this financial expansion, with North America currently holding a dominant 38% share of the total market as of 2026. This leadership is largely due to the region’s high concentration of medical technology giants and a healthcare infrastructure that is early to adopt breakthrough innovations. The presence of sophisticated insurance reimbursement models also plays a critical role, allowing for the rapid deployment of high-cost, high-impact devices such as leadless pacemakers and smart orthopedic implants. Furthermore, the United States serves as the primary engine for clinical trials, which accelerates the commercialization of new devices and maintains the region’s competitive edge. The synergy between academic research institutions and private capital continues to fuel a pipeline of next-generation solutions that define the global standard of care.

Europe follows closely with a 29% share of the market, characterized by a strong emphasis on clinical evidence and long-term patient safety protocols. While the regulatory landscape in Europe is rigorous, it provides a stable environment for manufacturers who can prove the efficacy of their devices within established public health systems. Meanwhile, the Asia-Pacific region is quickly closing the gap, currently accounting for 25% of the market and showing the highest growth rate among all geographic segments. This surge is driven by massive healthcare investments in China, Japan, and India, where aging populations and expanding middle classes are demanding better access to modern medical interventions. As these nations develop their domestic manufacturing capabilities, they are reducing their reliance on imports and becoming significant exporters of medical technology, reshaping the global competitive dynamic.

Primary Drivers: Catalysts for Industry Expansion

Demographic Realities: Impact of an Aging Population

One of the most significant engines driving this industry is the demographic shift often described as the “silver tsunami,” which refers to the rapidly aging global population. As life expectancy increases across the globe, there is a corresponding rise in chronic, age-related conditions that require surgical intervention to maintain a basic quality of life. Osteoarthritis, cardiovascular disease, and neurodegenerative disorders are becoming more prevalent, necessitating a higher volume of reconstructive and life-support implants. This demographic reality creates a sustained demand that is less sensitive to economic cycles, as the medical necessity for these devices often outweighs personal financial considerations. The elderly population today is more active than previous generations, which further increases the demand for durable implants that can withstand the rigors of an energetic lifestyle.

Cardiovascular disorders remain a primary cause of mortality worldwide, sustaining a massive demand for stents, heart valves, and implantable cardioverter defibrillators that can prevent sudden cardiac events. Simultaneously, rising obesity rates and sedentary lifestyles in developed nations have led to a surge in degenerative joint issues, particularly in the hip and knee. This has directly boosted the orthopedic segment, as more patients seek replacements to maintain their mobility and independence in their later years. The psychological shift toward proactive health management among the elderly also means that patients are seeking these interventions earlier in the disease progression. Consequently, manufacturers are focusing on developing implants that are not only more durable but also more biologically compatible to minimize the risk of late-stage complications in patients who may live for decades with their devices.

Clinical Innovations: Growth of Minimally Invasive Procedures

Beyond demographics, the growing preference for minimally invasive procedures is fundamentally reshaping the market landscape and expanding the pool of eligible patients. Modern surgical techniques allow for the implantation of complex devices through much smaller incisions, which significantly reduces patient trauma, minimizes the risk of post-operative infection, and accelerates recovery times. These technological advancements in delivery systems, such as transcatheter valve replacements and leadless cardiac monitors, have made life-altering treatments accessible to a wider demographic of patients. This includes individuals who might have been considered too high-risk or frail for traditional open-heart or open-joint surgeries just a few years ago. The reduction in hospital stay duration also appeals to healthcare providers looking to optimize bed turnover and reduce the total cost per procedure.

The evolution of delivery catheters and robotic-assisted surgical platforms has allowed surgeons to place implants with a level of precision that was previously unattainable. This high-degree of accuracy ensures better alignment and fixation, which are critical factors in the long-term success and longevity of an implant. As these minimally invasive tools become more standardized, they are being adopted by smaller, community-based hospitals and ambulatory surgical centers, further driving market penetration. The continuous innovation in materials science also complements these surgical techniques, as devices are being designed to be more flexible and compressible without losing their structural integrity. This synergy between surgical method and device design is a primary driver of the current growth cycle, as it aligns the interests of the patient, the surgeon, and the healthcare payer through improved clinical outcomes and efficiency.

Strategic Challenges: Navigating Barriers to Adoption

Economic Obstacles: Affordability and Healthcare Access

Despite the positive growth outlook, the total cost of care remains a significant barrier for many patients and healthcare systems worldwide. The expense of an implantable medical device includes not just the hardware itself but also the costs associated with specialized surgical expertise, high-tech diagnostic imaging, and long-term post-operative monitoring. In cost-sensitive markets or regions with limited insurance coverage, these financial requirements can lead to significant disparities in healthcare access, where only the most affluent populations can afford the latest innovations. Even in developed nations, the rising cost of medical technology is putting immense pressure on public and private payers to implement stricter cost-benefit analyses before approving new treatments. This creates a challenging environment for manufacturers who must prove that their devices provide substantial value over existing, cheaper alternatives.

The financial burden extends to the long-term maintenance and potential replacement of devices, which can involve additional surgeries and hospitalizations. For instance, while a sophisticated neurostimulator may offer excellent results for chronic pain, the need for battery replacements or lead adjustments can add substantial long-term costs. Manufacturers are responding by developing rechargeable systems and more durable components to extend the life of the device, but the initial price point remains a hurdle. Additionally, the global supply chain for high-end medical components is subject to fluctuations in material costs and geopolitical tensions, which can further drive up prices. For the market to reach its full potential, the industry must find ways to reduce production costs through automation and economies of scale, ensuring that life-saving technology is not restricted by a patient’s geographic location or socioeconomic status.

Regulatory Risks: Ensuring Safety and Cybersecurity

Regulatory scrutiny is another major factor that companies must navigate with extreme care, as these devices are often classified as high-risk due to their long-term or permanent placement inside the human body. Achieving market approval is a multi-year, multi-million-dollar endeavor that requires rigorous proof of safety, biocompatibility, and clinical efficacy through extensive human trials. Any changes in regulatory standards, such as the Medical Device Regulation (MDR) in Europe, can create high hurdles for new entrants and existing manufacturers alike, often leading to delays in product launches or the withdrawal of older devices from the market. This intense oversight is necessary to protect patient safety, but it also increases the cost of innovation and can limit the speed at which new, potentially superior technologies reach the clinical environment.

Furthermore, the rise of connected “smart” implants has introduced entirely new categories of risk, specifically regarding cybersecurity and data privacy. Because these devices transmit sensitive physiological data wirelessly, they are potential targets for unauthorized access or tampering by external actors. A breach in the security of a life-critical device like a pacemaker or an insulin pump could have catastrophic consequences for the patient. Consequently, manufacturers are now required to implement robust digital protections and encryption protocols that must be continuously updated to counter evolving cyber threats. This adds another layer of complexity to the design and maintenance of implantable devices, requiring a multidisciplinary approach that combines medical expertise with advanced software engineering. The balance between connectivity and security is one of the most critical challenges the industry faces as it moves toward a more digitized healthcare model.

Technological Renaissance: Smart Innovations and Design

Digital Integration: Connectivity and Real-Time Monitoring

The industry is currently experiencing a technological revolution characterized by the rise of smart implants that function as internal diagnostic tools. These devices are increasingly capable of transmitting real-time heart rhythm, blood pressure, or other physiological data directly to a physician’s smartphone or a centralized monitoring center. This shift toward connected health enables a proactive medical model where potential issues can be identified and addressed before they escalate into medical emergencies. For example, a modern cardiac monitor can alert a doctor to a minor arrhythmia days before the patient even feels a symptom, allowing for early pharmaceutical intervention that might prevent a stroke. This level of continuous oversight provides patients with a greater sense of security and significantly improves the quality of data available for clinical decision-making.

The integration of low-power Bluetooth and other wireless communication protocols allows these devices to operate for years without needing a battery change, making long-term monitoring feasible. This connectivity also facilitates the remote adjustment of device settings, reducing the need for patients to travel to specialized clinics for routine check-ups. In the field of orthopedics, “smart” knee and hip replacements are being tested with embedded sensors that track gait, range of motion, and load distribution. This data can be used to customize physical therapy programs and detect early signs of implant loosening or infection, potentially preventing the need for revision surgeries. As the ecosystem of wearable and implantable technology becomes more integrated, the data generated will likely play a key role in the development of personalized medicine, where treatments are adjusted in real-time based on the patient’s unique biological responses.

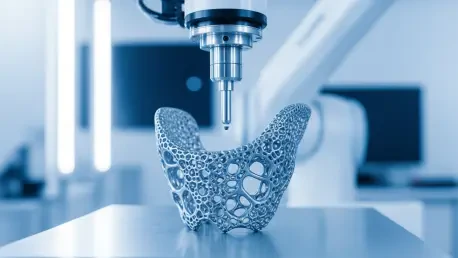

Manufacturing Precision: 3D Printing and Personalization

Personalization is another key trend that is revolutionizing the design and manufacturing of implantable devices, with 3D printing allowing for solutions tailored to a patient’s specific anatomy. Using high-resolution digital imaging from CT and MRI scans, manufacturers can produce orthopedic and dental solutions that fit perfectly and integrate more effectively with living bone tissue. This replaces the traditional “one-size-fits-all” approach, leading to better long-term stability, fewer post-operative complications, and a more natural feel for the patient. The ability to create complex, porous structures through additive manufacturing also encourages osseointegration, where the patient’s own bone grows into the implant, creating a much stronger and more durable bond than traditional cements or screws could ever provide.

Artificial intelligence plays a crucial role in this personalization process by optimizing the design of implants to maximize load-bearing capabilities and structural integrity while minimizing weight. AI algorithms can analyze thousands of anatomical variations to suggest the most effective implant shapes and materials for a specific patient’s bone density and activity level. This level of data-driven design is becoming the new standard for complex reconstructive surgeries, particularly in the spinal and cranial segments of the market where anatomical precision is paramount. Advances in biomaterials are also enhancing clinical outcomes, with the growing use of wear-resistant ceramics and bioresorbable polymers that dissolve safely after their therapeutic purpose is served. These innovations are being implemented with sub-millimeter precision thanks to robotic-assisted surgical platforms, which minimize human error and ensure the longevity of the device within the patient’s body.

Market Segmentation: Specialized Applications and Dynamics

Cardiovascular Trends: Innovation in Heart Health

The cardiovascular segment remains the largest part of the market as of 2026, currently accounting for approximately 32% of the total share and driving the majority of technological breakthroughs. Innovation in this area is moving rapidly toward leadless pacemakers and miniaturized monitors that provide high-resolution data without the complications associated with traditional wiring. These advancements are critical for managing the global burden of heart disease while minimizing the risk of infection and mechanical failure of the leads, which have historically been the weakest points in cardiac stimulation systems. The development of bioresorbable stents is also a major focus, as these devices provide the necessary support to a coronary artery during the healing process and then gradually disappear, leaving the vessel in a more natural state.

In addition to rhythm management, the structural heart segment is seeing a surge in innovation, particularly with transcatheter aortic valve replacement (TAVR) systems. These devices allow for the treatment of severe valve stenosis without the need for invasive open-heart surgery, significantly improving the prognosis for elderly patients. The market is also seeing the introduction of more sophisticated implantable cardioverter defibrillators (ICDs) that are smaller and more intelligent, capable of distinguishing between life-threatening arrhythmias and benign heart rate changes. As heart failure becomes more prevalent globally, the demand for ventricular assist devices and other mechanical circulatory supports is also on the rise. These technologies are increasingly being used as a “destination therapy” for patients who are not candidates for heart transplants, providing them with years of additional, high-quality life through advanced engineering.

Neurological Advancements: The Rise of Bioelectronic Medicine

Specialized categories like neurology are seeing some of the fastest growth in the industry, despite having a smaller total market share compared to the cardiovascular and orthopedic sectors. This segment includes deep brain stimulators (DBS) for the treatment of Parkinson’s disease and essential tremor, as well as spinal cord stimulators (SCS) for chronic pain management. The future of this field lies in bioelectronic medicine, where precisely targeted electrical impulses are used to treat conditions that were previously managed only with pharmaceutical interventions. This approach offers a more targeted therapeutic response with fewer systemic side effects, providing a new pathway for patients with treatment-resistant disorders. Researchers are also exploring the use of nerve stimulation for autoimmune diseases and gastrointestinal disorders, expanding the potential applications of neurological implants.

The development of brain-computer interfaces (BCI) represents the next frontier in this segment, with the potential to restore communication and mobility to patients with paralysis or severe neurological damage. While many of these technologies are still in the early stages of commercialization, the progress made by companies in 2026 has been substantial, with several systems entering advanced clinical trials. These devices use sophisticated sensors to detect neural activity and translate it into digital commands, allowing patients to control external devices or even their own limbs through stimulated muscle movement. The integration of artificial intelligence is essential here, as it allows the device to “learn” the patient’s unique neural patterns over time, improving accuracy and responsiveness. As bioelectronic medicine continues to mature, it is expected to become a cornerstone of neurological care, offering hope to millions of patients worldwide.

Competitive Environment: Regional Leadership and Corporate Strategy

Geographic Analysis: Dominance in Key Global Regions

The United States continues to lead the global market due to its high healthcare spending and robust appetite for medical innovation across both public and private sectors. American healthcare providers are among the first to integrate remote monitoring platforms and robotic-assisted surgical suites into their standard care models, creating a feedback loop that encourages further technological development. The region serves as a primary hub for research and development, with a regulatory environment that, while strict, offers pathways for the commercialization of breakthrough technologies through programs like the FDA’s Breakthrough Devices Program. This leadership is also supported by a vast network of venture capital and private equity firms that provide the necessary funding for early-stage startups to move from the laboratory to the clinical setting.

In Europe, Germany and the United Kingdom are the primary market drivers, with a strong emphasis on integrating cost-effective technologies into their universal healthcare systems. The focus here is often on long-term clinical data and the ability of a device to reduce the overall burden on the healthcare system by preventing complications and re-hospitalizations. Meanwhile, the Asia-Pacific region is becoming a major destination for medical tourism, offering high-quality implantation procedures at a fraction of the costs seen in Western nations. Countries like South Korea and Singapore are investing heavily in medical technology infrastructure, positioning themselves as regional leaders in high-tech surgical interventions. This global shift is forcing traditional market leaders to adapt their strategies, often leading to localized manufacturing and R&D centers to better serve the unique needs and regulatory requirements of different geographic markets.

Industry Consolidation: The Role of Strategic Acquisitions

The competitive environment is dominated by a few massive multinational conglomerates, including Medtronic, Abbott Laboratories, Johnson & Johnson, and Stryker, which maintain their leadership through strategic scale. These companies utilize their massive research and development budgets to stay at the cutting edge of the market, but they also rely heavily on the acquisition of smaller, specialized firms. By purchasing startups that focus on AI-driven diagnostics, new biomaterials, or novel surgical techniques, these industry giants are able to quickly integrate breakthrough technologies into their existing product portfolios. This strategy allows them to mitigate the risks associated with internal R&D while ensuring they remain competitive in a rapidly evolving technological landscape. Consolidation also provides these companies with the distribution networks and regulatory expertise needed to bring complex devices to a global audience.

Recent developments in 2024 and 2025 have seen the launch of a new generation of wireless cardiac monitors and neurotechnology that uses AI to “learn” a patient’s specific neural patterns in real-time. These milestones highlight a fundamental shift toward devices that are not just mechanical replacements but “biologically intelligent” systems that act as an extension of the patient’s own body. As companies continue to push the boundaries of what is possible, the line between a traditional medical device and a digital health platform is becoming increasingly blurred. The competitive landscape is now as much about software and data analytics as it is about hardware and surgical precision. This transition requires a new set of skills and partnerships, leading to more collaborations between traditional medical device manufacturers and big-tech firms specialized in data security and machine learning.

The global medical community recognized the critical need for a transition toward a more integrated and data-centric approach to implantable technology. Stakeholders successfully navigated the complexities of biocompatibility and digital security to deliver a new generation of devices that were both life-saving and proactively managed. The industry shifted its focus from the point of implantation to the long-term therapeutic journey, ensuring that every patient benefited from personalized design and continuous clinical oversight. By prioritizing the intersection of advanced materials and artificial intelligence, manufacturers established a foundation for a future where chronic conditions were managed with unprecedented precision. The commitment to reducing surgical trauma and enhancing device longevity resulted in a more resilient healthcare system that could effectively meet the demands of a growing and aging global population. Moving forward, the industry continued to build on these successes by fostering cross-disciplinary collaboration and maintaining a steadfast focus on the quality of human life.